EU ESG Regulations in 2026: What Companies Need to Prepare for Across Reporting, Supply Chains, Products, Claims, and Governance

2026 marks the point at which the EU ESG landscape is no longer defined primarily by reporting, but increasingly by a multi-functional compliance architecture with direct operational consequences.[1] It spans corporate disclosure, supply-chain due diligence, imports, product rules, environmental claims, and internal governance.

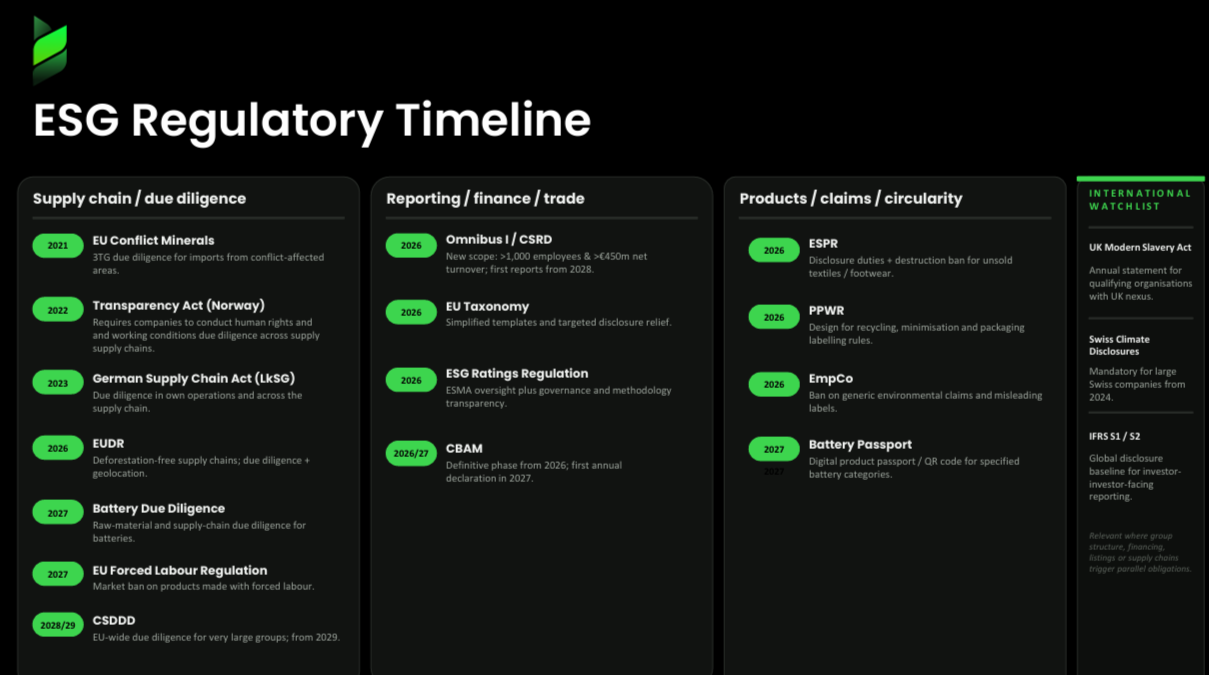

As illustrated in the timeline graphic below, the real challenge for companies is no longer only whether one directive applies, but how multiple regimes increasingly interact across the same underlying data, controls, and decisions.

Why 2026 matters

The significance of 2026 lies in the fact that several major EU frameworks no longer remain abstract policy developments, but begin to take effect through application dates, operational rollout, or concrete implementation requirements.

This includes the narrowed CSRD perimeter, the definitive phase of CBAM, the application of the Packaging and Packaging Waste Regulation, the application date of the ESG Ratings Regulation, and the application timeline of the Empowering Consumers for the Green Transition Directive.[2] In parallel, companies also need to prepare for the next wave of rules already visible on the horizon, including EUDR, the Batteries Regulation, the Forced Labour Regulation, and the later application of the narrowed CSDDD framework.[3]

1. Corporate reporting: CSRD still matters after simplification

The Corporate Sustainability Reporting Directive remains the central EU framework for sustainability reporting, even after the 2025–2026 Omnibus simplification package. The first wave of CSRD reports was published in 2025 for financial year 2024, confirming the shift of ESG disclosure into the management-report and assurance environment. The Stop-the-Clock Directive postponed certain reporting and due-diligence application dates, but it did not repeal the broader legal architecture.

Under the final 24 February 2026 Omnibus outcome, CSRD scope was narrowed to large undertakings with more than 1,000 employees and more than EUR 450 million net annual turnover.[4] That is a major perimeter change, but it does not make ESG data irrelevant for companies falling out of direct scope. Banks, customers, procurement processes, ratings ecosystems, and group-reporting demands can still require comparable, decision-useful, and defensible ESG information.

For companies that remain in scope, 2026 is primarily a controls-and-readiness year. Governance responsibilities, data ownership, internal controls, auditability, and management-report integration are likely to matter as much as the disclosure text itself.[5] For companies that fall outside direct scope, the practical question is whether a voluntary but structured reporting architecture is still needed to respond to lenders, customers, ratings providers, or parent-company requirements.

Another important reporting development in 2026 is the EU Taxonomy simplification package.[6] The Commission adopted a delegated act to simplify the content and presentation of Article 8 disclosures.[7] These simplification measures apply from 1 January 2026 for financial year 2025, although undertakings may choose to begin applying them from financial year 2026 instead.[8]

2. Supply chains: where ESG becomes operational control

The strongest operational ESG pressure in 2026 sits in the supply chain.[9] This is where sustainability moves from disclosure into evidence-based control over suppliers, imports, sourcing decisions, and risk handling.

The Carbon Border Adjustment Mechanism entered its definitive phase on 1 January 2026.[10] The Commission states that CBAM was deployed across Member States with interconnection between the CBAM Registry, customs systems, and validation processes for declarants.[11] For importers of in-scope goods, embedded carbon has therefore become a customs, procurement, and margin-management issue, not only a sustainability metric. The first annual declaration and certificate-related compliance cycle for 2026 imports will follow in 2027, which means supplier emissions data, methodology, and customs governance must already be working during 2026.

The Corporate Sustainability Due Diligence Directive also remains strategically important after narrowing.[12] Under the final 2026 Omnibus outcome, the threshold was raised to 5,000 employees and EUR 1.5 billion net worldwide turnover.[13] Transposition is due by 26 July 2028, and application starts from 26 July 2029 for the remaining very large groups in scope. Even with that narrower perimeter, the directive remains legally significant because it reinforces the expectation that companies identify, prevent, mitigate, and address adverse human-rights and environmental impacts in their chain of activities.

The Forced Labour Regulation adds a separate market-access risk.[14] Regulation (EU) 2024/3015 applies from 14 December 2027 and prohibits products made with forced labour from being placed on, made available in, or exported from the EU market. In practice, that increases the importance of supplier traceability, complaints handling, remediation logic, and evidence trails well before the formal application date.

The timeline also sits alongside earlier and parallel due-diligence regimes that continue to matter in practice. The EU Conflict Minerals Regulation still imposes due-diligence obligations for Union importers of tin, tantalum, tungsten, and gold from conflict-affected and high-risk areas. Germany’s Supply Chain Due Diligence Act remains relevant for companies with German operations or supply-chain exposure and has applied since 2023 to larger companies, with the threshold lowered from 2024.[15] For cross-border groups, the UK Modern Slavery Act and IFRS-linked investor expectations can also shape disclosure and due-diligence expectations beyond the minimum EU perimeter.[16]

3. Products and traceability: ESG moves down to item level

A second major 2026 theme is product-level ESG compliance. Here, companies increasingly need item-level, material-level, component-level, and origin-level data rather than broad policy statements.

The EU Deforestation Regulation applies from 30 December 2026 for large and medium operators and traders, and from 30 June 2027 for micro and small operators and traders.[17] Its practical core is due diligence supported by geolocation data and evidence that covered products are deforestation-free and legally produced. That makes ESG a sourcing and product-traceability issue rather than only a reporting issue.

The Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, entered into force on 11 February 2025 and applies from 12 August 2026.[18] It replaces Directive 94/62/EC from that date, subject to some exceptions. For companies, PPWR has implications far beyond packaging policy, because it brings legal consequences for design, minimisation, recyclability, labelling, and cross-functional data ownership between legal, procurement, operations, and product teams.

The Ecodesign for Sustainable Products Regulation is another foundational part of the 2026 compliance landscape.[19] It establishes the legal framework for future ecodesign requirements and the roll-out of Digital Product Passports through delegated acts. It also already contains certain immediate rules, including the destruction ban for unsold textiles and footwear for relevant operators.This means the Digital Product Passport should no longer be treated as a distant concept, but as part of a live legal architecture that will increasingly affect product data and lifecycle transparency.

The Batteries Regulation adds another phased product-compliance layer.[20] From 18 February 2027, all batteries covered by the Regulation must be marked with a QR code as described in Annex VI.[21] The same framework also establishes broader obligations around battery information, sustainability, and due-diligence structures. From a compliance perspective, the critical point is that battery obligations are phased and category-specific, so carbon footprint, passport, recycled-content, labelling, and due-diligence requirements should be mapped carefully by battery type and operator role.

4. Claims, ratings, and credibility

Another important 2026 front is the regulation of sustainability claims, methodologies, and external ESG signalling.[22] The Empowering Consumers for the Green Transition Directive must be transposed by 27 March 2026 and applied from 27 September 2026.[23] Its practical effect is to tighten the legal standard for environmental marketing claims and misleading sustainability labels, making substantiation, documentation, and evidence retention more important for legal and marketing teams.

The ESG Ratings Regulation also becomes operational in 2026.[24] ESMA states that the date of application is 2 July 2026. ESMA also states that ESG rating providers will need to consider notifying the authority if they wish to continue operating in the Union and that ESMA will assume direct supervisory responsibilities under the regime. For companies, that does not create a CSRD-style reporting duty, but it does raise expectations around consistency, methodology transparency, governance, and responsiveness in capital-market interactions.

5. Governance and AI: ESG compliance now depends on system quality

In 2026, ESG is also a governance and systems issue. Many companies now use AI in supplier screening, due-diligence workflows, document extraction, risk scoring, data classification, and reporting support.[25] Once such systems influence regulated processes, evidence files, or disclosures, model governance and control quality become part of ESG compliance itself.

The AI Act entered into force on 1 August 2024 and is described by the Commission as becoming fully applicable on 2 August 2026, with exceptions and staggered dates for parts of the regime.[26] The Commission also notes that high-risk AI systems embedded into regulated products have an extended transition period until 2 August 2027.[26] At the same time, the Digital Omnibus on AI proposes linking some high-risk obligations to the availability of standards and support tools. The Commission’s digital policy materials explain that this is intended to smooth implementation and may affect how companies interpret the operational timeline for certain high-risk use cases.

For companies using AI in ESG-relevant processes, the practical implication is clear. Documentation, oversight, accountability, data quality controls, escalation paths, and human review should be built into sustainability-related workflows before those systems become deeply embedded in legal or reporting processes.

6. What will hit hardest in practice

In practice, the most significant consequence of the 2026 EU ESG landscape is not the application of a single regulation, but the growing interaction between several regimes that rely on overlapping datasets, controls, and governance structures. The same information may increasingly be used across sustainability reporting, customs processes, supply-chain due diligence, product compliance, and claims substantiation.

The operational relevance of this shift differs by industry.

For import-intensive sectors such as metals, chemicals, construction materials, fertilisers, and electricity-related value chains, CBAM creates a direct interface between emissions data, customs declarations, supplier methodology, and cost exposure.

For consumer goods, food, retail, furniture, rubber, and wood-based sectors, EUDR increases the importance of origin-level traceability, geolocation evidence, and supplier due diligence.

For packaging-heavy sectors such as FMCG, food and beverage, pharmaceuticals, e-commerce, and logistics, PPWR creates immediate implications for packaging design, recyclability, labelling, and cross-border market requirements.

Product-intensive sectors such as electronics, appliances, automotive, textiles, and industrial manufacturing are likely to feel increasing pressure from ecodesign rules and the gradual rollout of Digital Product Passports.

Battery-related obligations are particularly relevant for automotive, mobility, electronics, and energy-storage value chains.

A further distinction concerns capital-market-facing and brand-facing industries. Listed companies, financial-market participants, and businesses exposed to ratings-based scrutiny are likely to experience stronger pressure around methodological consistency, data quality, and responsiveness toward ESG ratings providers.

At the same time, sectors with high consumer visibility such as retail, consumer products, mobility, and household goods face greater legal and reputational sensitivity around environmental claims and the substantiation of sustainability-related communications. In these sectors, weak coordination between legal, marketing, sustainability, procurement, and product teams can create material compliance risk even where the underlying sustainability strategy is relatively mature.

Against this background, one of the most significant organisational risks is fragmented ownership. In many companies, supplier data, emissions logic, product specifications, packaging information, and legal review remain distributed across separate functions. The practical challenge in 2026 is therefore less about collecting additional disclosures in isolation and more about building integrated governance over shared compliance data. Companies that treat reporting, sourcing, customs, product compliance, and claims governance as separate workstreams are more likely to face duplication, inconsistency, and evidentiary gaps than companies that organise these topics around common data structures, controls, and accountability.

7. What comes next

The pressure does not disappear after 2026. The EUDR expands to micro and small operators on 30 June 2027.The battery QR-code requirement starts on 18 February 2027. The Forced Labour Regulation applies from 14 December 2027. The narrowed CSDDD timetable points to transposition by 26 July 2028 and application from 26 July 2029.

ETS2 also matters for companies exposed to fuel, mobility, logistics, or building-related cost pass-through.The Commission states that regulated entities will have to surrender allowances from 2028 once verified annual emissions have been reported. That makes carbon cost a more direct economic variable for additional sectors beyond the current EU ETS perimeter.[27]

8. Conclusion

The most accurate framing for 2026 is not that the EU is stepping back from ESG regulation. It is simplifying parts of the perimeter for certain reporting and due-diligence rules while operationalising harder obligations around imports, product traceability, packaging, claims, ratings, and governance.

For companies across industries, the defensible response is therefore not to focus only on whether formal CSRD scope still applies, but to identify where ESG data has already become compliance-critical across reporting, sourcing, customs, product design, marketing, financing, and AI-enabled workflows.

Footnotes

[1] Council of the European Union, “Council signs off simplification of sustainability reporting and due diligence requirements to boost EU competitiveness,” press release, February 24, 2026, https://www.consilium.europa.eu/en/press/press-releases/2026/02/24/council-signs-off-simplification-of-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness (accessed March 23, 2026).

European Commission, “CBAM successfully entered into force on 1 January 2026,” news item, January 14, 2026, https://taxation-customs.ec.europa.eu/news/cbam-successfully-entered-force-1-january-2026-2026-01-14_en (accessed March 23, 2026).

European Securities and Markets Authority, “ESG Rating Providers,” supervision page, 2026, https://www.esma.europa.eu/esmas-activities/investors-and-issuers/esg-rating-providers (accessed March 23, 2026).

EUR-Lex, “Packaging and packaging waste,” summary of Regulation (EU) 2025/40, September 17, 2025, https://eur-lex.europa.eu/EN/legal-content/summary/packaging-and-packaging-waste.html (accessed March 23, 2026).

[2] Council of the European Union, “Council signs off simplification of sustainability reporting and due diligence requirements to boost EU competitiveness,” press release, February 24, 2026, https://www.consilium.europa.eu/en/press/press-releases/2026/02/24/council-signs-off-simplification-of-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness (accessed March 23, 2026).

European Commission, “CBAM successfully entered into force on 1 January 2026,” news item, January 14, 2026, https://taxation-customs.ec.europa.eu/news/cbam-successfully-entered-force-1-january-2026-2026-01-14_en (accessed March 23, 2026).

EUR-Lex, “Packaging and packaging waste,” summary of Regulation (EU) 2025/40, September 17, 2025, https://eur-lex.europa.eu/EN/legal-content/summary/packaging-and-packaging-waste.html (accessed March 23, 2026).

European Securities and Markets Authority, “ESG Rating Providers,” supervision page, 2026, https://www.esma.europa.eu/esmas-activities/investors-and-issuers/esg-rating-providers (accessed March 23, 2026).

European Parliament and Council of the European Union, “Directive (EU) 2024/825 as regards empowering consumers for the green transition,” EUR-Lex, February 28, 2024, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32024L0825 (accessed March 23, 2026).

[3] European Commission, “Regulation on Deforestation-free products,” policy page, 2026, https://environment.ec.europa.eu/topics/forests/deforestation/regulation-deforestation-free-products_en (accessed March 23, 2026).

EUR-Lex, “Sustainability rules for batteries and waste batteries,” summary of Regulation (EU) 2023/1542, 2025, https://eur-lex.europa.eu/EN/legal-content/summary/sustainability-rules-for-batteries-and-waste-batteries.html (accessed March 23, 2026).

European Parliament and Council of the European Union, “Regulation (EU) 2024/3015 on prohibiting products made with forced labour on the Union market,” EUR-Lex, November 27, 2024, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ%3AL_202403015 (accessed March 23, 2026).

European Parliament and Council of the European Union, “Directive (EU) 2024/1760 on corporate sustainability due diligence,” EUR-Lex, June 13, 2024, https://eur-lex.europa.eu/eli/dir/2024/1760/oj/eng (accessed March 23, 2026).

Council of the European Union, “Council signs off simplification of sustainability reporting and due diligence requirements to boost EU competitiveness,” press release, February 24, 2026, https://www.consilium.europa.eu/en/press/press-releases/2026/02/24/council-signs-off-simplification-of-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness (accessed March 23, 2026).

[4] Council of the European Union, “Council signs off simplification of sustainability reporting and due diligence requirements to boost EU competitiveness,” press release, February 24, 2026, https://www.consilium.europa.eu/en/press/press-releases/2026/02/24/council-signs-off-simplification-of-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness (accessed March 23, 2026).

[5] IFRS Foundation, IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information, 2023, https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s1-general-requirements/ (accessed March 23, 2026).

IFRS Foundation, IFRS S2 Climate-related Disclosures, 2023, https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s2-climate-related-disclosures/ (accessed March 23, 2026).

[6] European Commission, “Commission to cut EU taxonomy red tape for companies,” publication, July 4, 2025, https://finance.ec.europa.eu/publications/commission-cut-eu-taxonomy-red-tape-companies_en (accessed March 23, 2026).

[7] European Commission, “Commission to cut EU taxonomy red tape for companies,” publication, July 4, 2025, https://finance.ec.europa.eu/publications/commission-cut-eu-taxonomy-red-tape-companies_en (accessed March 23, 2026).

[8] European Commission, “Commission to cut EU taxonomy red tape for companies,” publication, July 4, 2025, https://finance.ec.europa.eu/publications/commission-cut-eu-taxonomy-red-tape-companies_en (accessed March 23, 2026).

[9] European Commission, “Carbon Border Adjustment Mechanism,” policy page, 2026, https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en (accessed March 23, 2026).

European Parliament and Council of the European Union, “Directive (EU) 2024/1760 on corporate sustainability due diligence,” EUR-Lex, June 13, 2024, https://eur-lex.europa.eu/eli/dir/2024/1760/oj/eng (accessed March 23, 2026).

OECD, OECD Due Diligence Guidance for Responsible Business Conduct (Paris: OECD Publishing, 2018), https://www.oecd.org/investment/due-diligence-guidance-for-responsible-business-conduct.htm (accessed March 23, 2026).

[10] European Commission, “CBAM successfully entered into force on 1 January 2026,” news item, January 14, 2026, https://taxation-customs.ec.europa.eu/news/cbam-successfully-entered-force-1-january-2026-2026-01-14_en (accessed March 23, 2026).

[11] European Commission, “CBAM successfully entered into force on 1 January 2026,” news item, January 14, 2026, https://taxation-customs.ec.europa.eu/news/cbam-successfully-entered-force-1-january-2026-2026-01-14_en (accessed March 23, 2026).

European Commission, “Carbon Border Adjustment Mechanism,” policy page, 2026, https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en (accessed March 23, 2026).

[12] Council of the European Union, “Council and Parliament strike a deal to simplify sustainability reporting and due diligence requirements and boost EU competitiveness,” press release, December 9, 2025, https://www.consilium.europa.eu/en/press/press-releases/2025/12/09/council-and-parliament-strike-a-deal-to-simplify-sustainability-reporting-and-due-diligence-requirements-and-boost-eu-competitiveness (accessed March 23, 2026).

European Parliament and Council of the European Union, “Directive (EU) 2024/1760 on corporate sustainability due diligence,” EUR-Lex, June 13, 2024, https://eur-lex.europa.eu/eli/dir/2024/1760/oj/eng (accessed March 23, 2026).

[13] Council of the European Union, “Council signs off simplification of sustainability reporting and due diligence requirements to boost EU competitiveness,” press release, February 24, 2026, https://www.consilium.europa.eu/en/press/press-releases/2026/02/24/council-signs-off-simplification-of-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness (accessed March 23, 2026).

Council of the European Union, “Council and Parliament strike a deal to simplify sustainability reporting and due diligence requirements and boost EU competitiveness,” press release, December 9, 2025, https://www.consilium.europa.eu/en/press/press-releases/2025/12/09/council-and-parliament-strike-a-deal-to-simplify-sustainability-reporting-and-due-diligence-requirements-and-boost-eu-competitiveness (accessed March 23, 2026).

[14] European Parliament and Council of the European Union, “Regulation (EU) 2024/3015 on prohibiting products made with forced labour on the Union market,” EUR-Lex, November 27, 2024, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ%3AL_202403015 (accessed March 23, 2026).

OECD, OECD Due Diligence Guidance for Responsible Business Conduct (Paris: OECD Publishing, 2018), https://www.oecd.org/investment/due-diligence-guidance-for-responsible-business-conduct.htm (accessed March 23, 2026).

[15] German Federal Office for Economic Affairs and Export Control (BAFA), “Information on the Supply Chain Act,” 2026, https://www.bafa.de/DE/Lieferketten/Multilinguales_Angebot/multilinguales_angebot_node.html (accessed March 23, 2026).

OECD, OECD Due Diligence Guidance for Responsible Business Conduct (Paris: OECD Publishing, 2018), https://www.oecd.org/investment/due-diligence-guidance-for-responsible-business-conduct.htm (accessed March 23, 2026).

Note: your source set still does not include a dedicated source for the EU Conflict Minerals Regulation itself.

[16] UK Parliament, “Modern Slavery Act 2015, section 54,” 2015, https://www.legislation.gov.uk/ukpga/2015/30/section/54 (accessed March 23, 2026).

IFRS Foundation, IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information, 2023, https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s1-general-requirements/ (accessed March 23, 2026).

IFRS Foundation, IFRS S2 Climate-related Disclosures, 2023, https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s2-climate-related-disclosures/ (accessed March 23, 2026).

[17] European Commission, “Regulation on Deforestation-free products,” policy page, 2026, https://environment.ec.europa.eu/topics/forests/deforestation/regulation-deforestation-free-products_en (accessed March 23, 2026).

European Commission, “Staff working document on EUDR implementation support,” February 12, 2026, https://environment.ec.europa.eu/document/download/c5a15594-3513-441c-978d-e5bc4bc26b53_en?filename=SWD_2026_66_1_EN_document_travail_service_part1_FINAL.pdf (accessed March 23, 2026).

[18] EUR-Lex, “Packaging and packaging waste,” summary of Regulation (EU) 2025/40, September 17, 2025, https://eur-lex.europa.eu/EN/legal-content/summary/packaging-and-packaging-waste.html (accessed March 23, 2026).

EUR-Lex, “Regulation (EU) 2025/40 on packaging and packaging waste,” summary page, September 17, 2025, https://eur-lex.europa.eu/legal-content/EN/LSU/?uri=CELEX%3A32025R0040 (accessed March 23, 2026).

[19] European Parliament and Council of the European Union, “Regulation (EU) 2024/1781 establishing a framework for the setting of ecodesign requirements for sustainable products,” EUR-Lex, June 13, 2024, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ%3AL_202401781 (accessed March 23, 2026).

European Commission, “Staff working document on digital product passport and related circularity architecture,” EUR-Lex, December 10, 2025, https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX%3A52025SC0990 (accessed March 23, 2026).

[20] EUR-Lex, “Sustainability rules for batteries and waste batteries,” summary of Regulation (EU) 2023/1542, 2025, https://eur-lex.europa.eu/EN/legal-content/summary/sustainability-rules-for-batteries-and-waste-batteries.html (accessed March 23, 2026).

European Parliament and Council of the European Union, “Regulation (EU) 2023/1542 concerning batteries and waste batteries,” EUR-Lex, July 12, 2023, https://eur-lex.europa.eu/eli/reg/2023/1542/oj/eng (accessed March 23, 2026).

[21] EUR-Lex, “Sustainability rules for batteries and waste batteries,” summary of Regulation (EU) 2023/1542, 2025, https://eur-lex.europa.eu/EN/legal-content/summary/sustainability-rules-for-batteries-and-waste-batteries.html (accessed March 23, 2026).

European Parliament and Council of the European Union, “Regulation (EU) 2023/1542 concerning batteries and waste batteries,” EUR-Lex, July 12, 2023, https://eur-lex.europa.eu/eli/reg/2023/1542/oj/eng (accessed March 23, 2026).

[22] European Parliament and Council of the European Union, “Directive (EU) 2024/825 as regards empowering consumers for the green transition,” EUR-Lex, February 28, 2024, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32024L0825 (accessed March 23, 2026).

European Securities and Markets Authority, “ESG Rating Providers,” supervision page, 2026, https://www.esma.europa.eu/esmas-activities/investors-and-issuers/esg-rating-providers (accessed March 23, 2026).

[23] European Parliament and Council of the European Union, “Directive (EU) 2024/825 as regards empowering consumers for the green transition,” EUR-Lex, February 28, 2024, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32024L0825 (accessed March 23, 2026).

[24] European Securities and Markets Authority, “ESG Rating Providers,” supervision page, 2026, https://www.esma.europa.eu/esmas-activities/investors-and-issuers/esg-rating-providers (accessed March 23, 2026).

European Securities and Markets Authority, “New Supervisory and Oversight Mandates,” 2026, https://www.esma.europa.eu/esmas-activities/new-supervisory-and-oversight-mandates (accessed March 23, 2026).

[25] European Commission, “AI Act,” policy page, February 2, 2025, https://digital-strategy.ec.europa.eu/en/policies/regulatory-framework-ai (accessed March 23, 2026).

European Commission, “Navigating the AI Act,” FAQ, January 28, 2026, https://digital-strategy.ec.europa.eu/en/faqs/navigating-ai-act (accessed March 23, 2026).

[26] European Commission, “AI Act,” policy page, February 2, 2025, https://digital-strategy.ec.europa.eu/en/policies/regulatory-framework-ai (accessed March 23, 2026).

European Commission, “Navigating the AI Act,” FAQ, January 28, 2026, https://digital-strategy.ec.europa.eu/en/faqs/navigating-ai-act (accessed March 23, 2026).

European Commission, “Digital Omnibus on AI Regulation Proposal,” November 19, 2025, https://digital-strategy.ec.europa.eu/en/library/digital-omnibus-ai-regulation-proposal (accessed March 23, 2026).

European Commission, “An agile Digital Rulebook for the EU,” policy page, November 19, 2025, https://digital-strategy.ec.europa.eu/en/policies/digital-rulebook (accessed March 23, 2026).

European Commission, “Standardisation of the AI Act,” policy page, March 11, 2026, https://digital-strategy.ec.europa.eu/en/policies/ai-act-standardisation (accessed March 23, 2026).

[27] European Commission, “ETS2: buildings, road transport and additional sectors,” policy page, 2026, https://climate.ec.europa.eu/eu-action/carbon-markets/ets2-buildings-road-transport-and-additional-sectors_en (accessed March 23, 2026).